The state of publisher ad revenue

The Rebooting partnered with Permutive, the audience platform used by publishers to increase their revenue, to survey The Rebooting's audience of publishing executives in order to understand the health of their ad businesses amid marketplace turbulence. The findings in this report are based off of 99 publishing executives surveyed as well as interviews with leading executives in the ecosystem.

Thank you to David Kaplan for collaborating on this report, and to Christine Cook, Sara Badler, Brian Wieser, David Cohen and Joe Root for contributing their perspectives.

Introduction

The state of digital advertising has never been more in flux. Privacy restrictions and the drawn-out phaseout of the third-party cookie, an unlikely bulwark of open web advertising, has thrown the market into chaos.

Publishers have seen their ad businesses go through gyrations in the post-pandemic era, with the sugar high of 2021 giving way to rough conditions the past two years as they’ve been caught between declines in social and search referral traffic coupled with continued shifts to one-to-one targeted advertising offered by platforms and an influx of retail media players enticing advertisers with the promise of closed-loop attribution.

WARC Media has forecast that global ad spend will surpass $1 trillion for the first time for a gain of 8.2% over 2023. Yet WARC expects “content media owners,” which includes TV, publishing, audio and cinema, are expected to net just 27.2% of all global ad investment in this year, a decline from 71% a decade ago.

The Rebooting partnered with Permutive to understand the state of ad revenue growth at publishers. We surveyed 99 digital publishers to get a health check of their ad businesses as we near the midpoint of 2024. In particular, we wanted to understand better how the mix of their advertising businesses is changing.

What we found is that publisher ad businesses are in flux: traffic declines are looming large and budgets are being eroded by new competition from retail media offerings’ bulletproof attribution. But many publishers are finding a resilient business that is shifting from an arm’s length relationship with advertisers to a direct one.

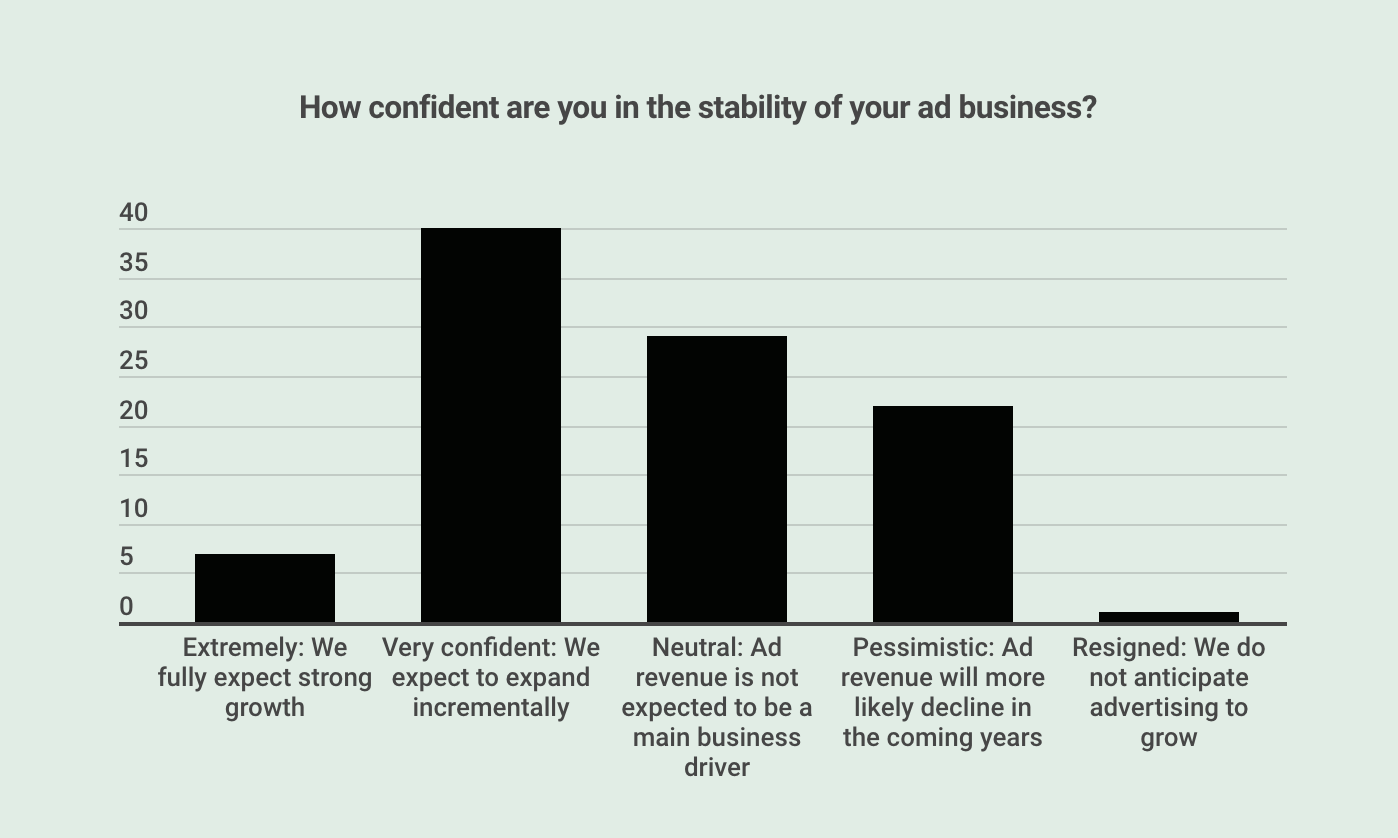

What we discovered is that after a rough couple of years, publishers are expressing cautious confidence in their current advertising revenue models. Few are expecting a return to the Roaring ‘20s days of 2021; but two-out-of-five publishers expressed confidence in returning to growth this year.

Tempered optimism

The glass is half-full for publishers gearing up for the back half of the year.

While just 7% are extremely bullish about achieving strong revenue growth this year, 40% of Rebooting survey respondents identified themselves as “very confident” of incremental gains.

Madison & Wall’s Brian Wieser, a media and advertising industry analyst, recently upgraded his previous November ad spending forecast in light of improvements in the U.S. economy. He’s calling for 5.6% ad industry growth in 2024, up from a prior 5.2% annual growth forecast. First-quarter ad industry revenue should rise 8%, Wieser said, up from his prior forecast calling for 7% growth.

Given the perpetually gloomy mood of publishers, those numbers count as optimism. To put the mood in additional context, 22% think ad dollars will drop in the next few years, while just one single respondent expressed no hope about an advertising upswing.

“The opportunity is up to the publisher to find holes in the market where they can make money,” said Wieser.

It’s often said that flat is the new up in digital advertising. After all, even a standout like The New York Times is seeing just 2.9% growth in its digital ad business. Most of its revenue growth is coming from its subscription bundle.

Our survey found reasons for optimism. Among respondents to our survey, over three quarters expect positive results for their ad businesses this year.

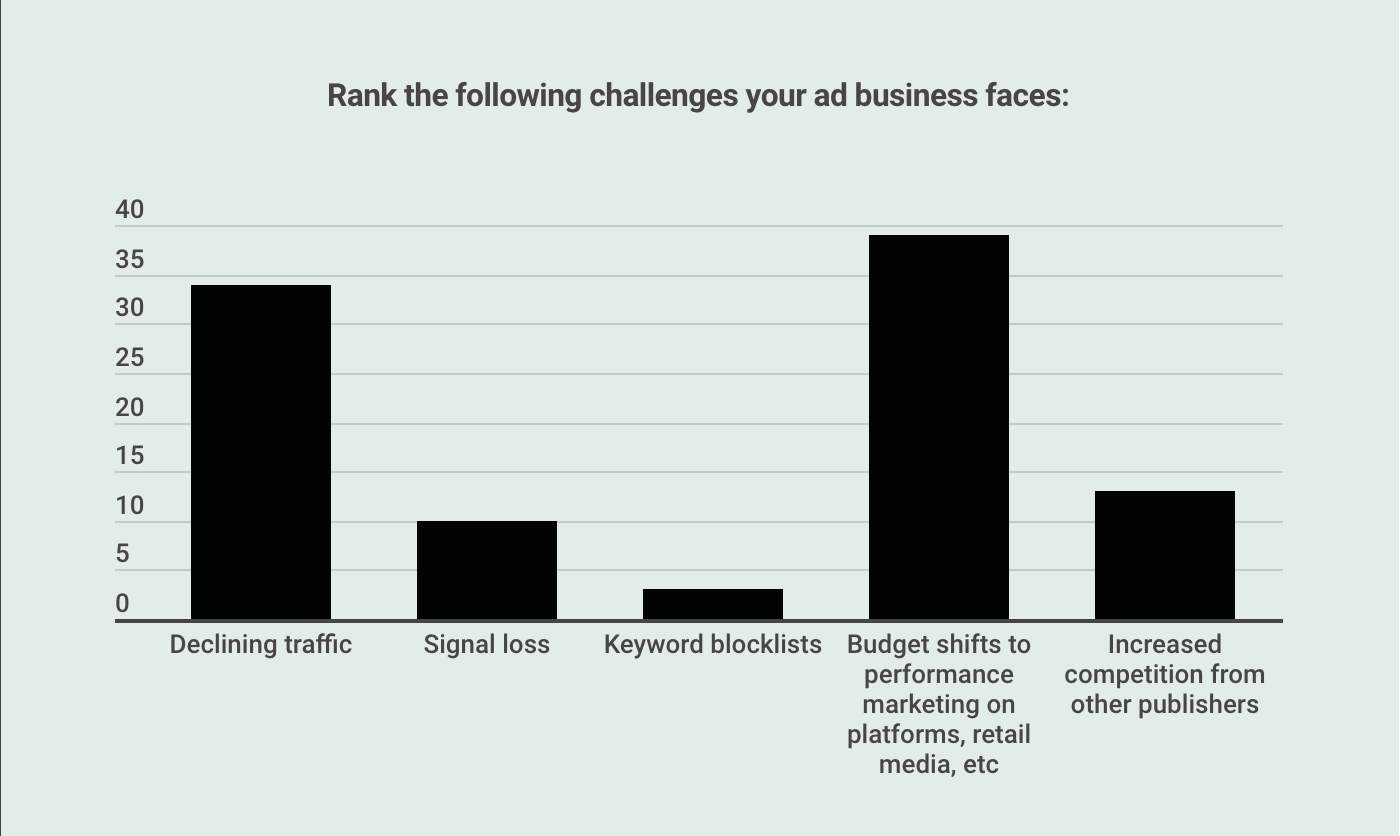

The biggest ad challenge for publishers turns out to be distribution. Many digital publishers have relied on search and social for the majority of their traffic, and that’s been in decline. The advent of AI search is not likely to reverse that trend, either.

Over a third cited declining traffic as their biggest challenge facing their digital ad business, far outranking signal loss and keyword blocklists.

“They dropped us as publishers; we had a supply chain wake up call,” said Christine Cook, global chief revenue officer at Bloomberg Media. “That forced us to have a better supply chain in terms of having more direct relationships with our audiences and advertisers.”

The bigger challenge cited by publishers arose from competition from non-publishers: platforms and retail media. Much of that is due to the enticing offer of closed-loop attribution that will prove to advertisers their ads resulted in sales.

New identity solutions are presented as the solution for this problem, only the “solution” is a Band-Aid on a gaping wound.

“What publishers are completely unaware of is that there's 70% of traffic where CPMs are less than $1 right now,” Root said. “The bottom line is that identity does not equal addressability. Anyone who beats that drum is going to kill the publisher industry.

The pendulum in media tends to swing wildly, and the current momentum is toward direct relationships.

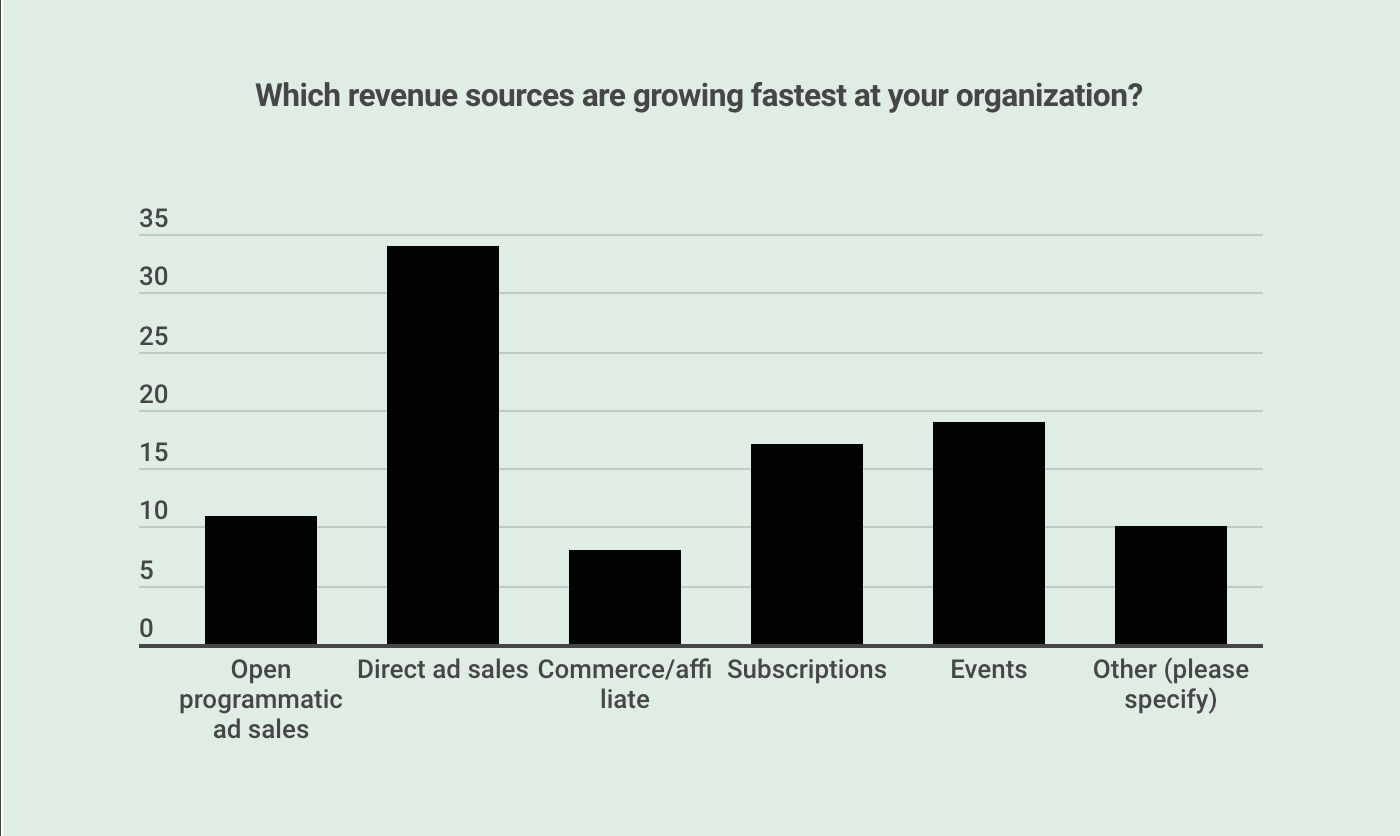

The Rebooting’s survey participants pointed to direct ad sales (34%) and subscriptions (17%) are among the fastest-growing revenue sources for publishers. These far outpaced open programmatic (11%) as a growth area.

Sara Badler, who recently joined Morning Brew in December as chief commercial officer after serving five years as chief revenue officer for Dotdash Meredith, senses a shift in many advertisers that want to work directly with trusted partners rather than the time-worn “see a cookie, hit a cookie” approach popularized by open programmatic advertising systems.

“It’s been energizing these past five months at Morning Brew as we continuously tap into several revenue streams, at a time when many marketers are looking to spend beyond programmatic, which I hear repeatedly.“

Digging deeper, about 51% of publishers who responded to the survey reported that 75%-100% of their ad revenue is direct sold.

Direct sold advertising, including programmatic guaranteed and private marketplace sales, are expanding at a majority of the publishers we surveyed (63%). In fact, a quarter of respondents reported growth exceeding 20%.

“Direct and open are these two extremes,” Root said. “In the middle sits more of a hybrid of those two. It requires a relationship with the agency, with the advertiser, with the retailer, but it's not done through the IO, it's not on a campaign-by-campaign basis. It is an always alive, always-on type of relationship powered by the publisher's understanding of the audience and the inventory which they have.”

Overall, programmatic continues to grow and now represents more than $114 billion in ad revenue, according to the IAB. However, IAB CEO David Cohen noted that activity in these online marketplaces is growing at a slower pace than previous years.

Not surprisingly given the greater focus on direct, respondents found open programmatic ad revenue delivering “mixed performance”; 13% saw gains of just over 20%, while 7% experienced declines over 20%.

Wieser said that the open web is dealing with significant challenges, chief among them being the signal loss associated with the slow death of third-party cookies and the rise of made-for-advertising sites.

Roughly 38% of the participants in The Rebooting's survey, many of whom responded shortly after Google announced it would delay the discontinuation of tracking pixels in its Chrome browser until 2025, indicated that the impact of phasing out third-party cookies would be moderate. However, another 28% view the eventual demise of cookies as a high risk. And yet, just 10 percent of respondents cited signal loss as their greatest challenge.

Conclusion

Publishing is entering a new phase with more competition than ever before. No longer are their peers the biggest rivals. Advertisers have a pot of money, and anyone getting an allocation is a competitor. Increasingly, the budgets that were going to publishers are being chipped away by non-publishers.

This is the reality of the Information Space. AI is looming as a major challenge, further eroding traffic to publishers and emphasizing again the need for them to reorient their businesses, as much as possible, to a North Star of direct relationships. That means with audiences and advertisers.

“Publishers’ competition is that dollars are leaving the open web and going into CTV, into retail media and social media,” said Permutive’s Root. “If publishers realize that they have the power, if they all tell the same story, then there's an opportunity to win.”